• Der Wirtschaftsaufschwung, der 2021 einsetzte und sich in den ersten Monaten des Jahres 2022 fortsetzte, führte zusammen mit angebotsseitigen Beschränkungen im Transportsektor zu einem Anstieg der Frachtraten im Seeverkehr und damit zu einer höheren Inflation.

• Der russische Angriffskrieg gegen die Ukraine führte zu einem weiteren Anstieg der Rohstoffpreise und zur Unsicherheit über das künftige Wirtschaftswachstum. Die Öl- und Gaspreise werden in 2022 voraussichtlich um 55% bzw. 147% an Wert gewinnen. Die Kohlenachfrage und damit die Kohlepreise werden 2022 aufgrund des europäischen Embargos für russische Kohle ebenfalls stark ansteigen.

• Für das Jahr 2022 wird ein Rückgang des BIP im Euroraum um 2,8% erwartet, vorausgesetzt, der Krieg bleibt auf die Ukraine beschränkt.

Das Jahr 2021 und der Beginn des Jahres 2022 zeigten eine stabile Erholung der Weltwirtschaft von der Pandemie. Dennoch hat der russische Angriffskrieg gegen die Ukraine1 zu einer erheblichen Verlangsamung des erwarteten Wachstums und zu einer kostspieligen humanitären Krise geführt.

Bereits im Jahr 2021 traten im Verkehrssektor angebotsseitige Beschränkungen in Form von überlasteten Seehäfen und Seeschifffahrtswegen auf. Zusammen mit der raschen Erholung im Jahr 2021 führten diese Faktoren zu einem Anstieg der Frachtraten im Seeverkehr und damit zu einem weiteren Anstieg der Inflationsraten.2

Infolge des Krieges wurden die ukrainischen Seehäfen geschlossen, wodurch die Ausfuhr von ukrainischem Getreide und anderen Rohstoffen blockiert wurde. Auch der Handel und die Warenströme (z. B. Kohle) aus Russland wurden stark eingeschränkt.

Die gegen Russland verhängten Handels- und Finanzsanktionen führten zu Einschränkungen bei der Energieversorgung der mittel- und westeuropäischen Länder, wodurch sich der Inflationstrend noch weiter verstärkte. Die Rohstoffpreise, insbesondere auf dem Lebensmittel- und Energiemarkt, steigen rasant an.

Das globale Wachstum (BIP) wird sich von schätzungsweise 6,1% im Jahr 2021 auf 3,6% in den Jahren 2022 und 2023 abschwächen. Diese Prognose geht davon aus, dass der Krieg auf die Ukraine beschränkt bleibt. Das Wachstum des Welthandels dürfte sich insbesondere im Jahr 2022 von schätzungsweise 10,1% im Jahr 2021 auf 5,0% im Jahr 2022 und weiter auf 4,4% im Jahr 2023 abschwächen.

Das Wachstum des Bruttoinlandsprodukts (BIP) der Eurozone wurde auf 2,8% nach unten korrigiert und liegt damit 1,1 Prozentpunkte unter der Prognose vom Januar 2022. Die Wirtschafts- und Geldpolitik steht vor einem schwierigen Kompromiss zwischen der Bekämpfung der Inflation und der Steigerung des Wirtschaftswachstums. Die Bekämpfung der Inflation erfordert eine Anhebung der Zinssätze, was jedoch höhere Finanzierungskosten und damit geringere private Investitionen und ein niedrigeres Wachstum bedeuten würde.

ABBILDUNG 1: PROZENTUALE VERÄNDERUNG DES BIP, KONSTANTE PREISE (IN %)

Quelle: IMF World Economic Outlook Database, Outlook April 2022

HANDEL

Durch den Krieg in der Ukraine werden die Handelsströme zunehmend gestört. Unterbrechungen der Lieferketten und den Mangel an Komponenten für die industrielle Produktion gab es bereits vor dem Krieg in der Ukraine. Dies schadet einigen Branchen, darunter auch der Automobilindustrie.

Diese Störung geht über Rohstoffe hinaus: Ein Beispiel ist die Produktion von Neongas, die sich in Russland und der Ukraine konzentriert. Neongas wird für die Herstellung von Halbleitern aus Silizium benötigt und ist daher für die Automobil-, Elektronik- und IT-Industrie unerlässlich. Darüber hinaus ist die weltweite Autoproduktion in hohem Maße von einem elektronischen Bordnetz abhängig, das in der Ukraine hergestellt wird, sowie von Metallen wie Palladium und Nickel, die in Russland produziert werden.

Eine wichtige wirtschaftliche Folge der Unterbrechung der Handelsströme ist, dass die Preise für fast alle Arten von Rohstoffen steigen. Dies betrifft nicht nur Getreide (auf Russland und die Ukraine entfallen rund 30% der weltweiten Weizenexporte), sondern auch Kohle, Rohöl, Mineralien und Metalle.

ROHSTOFFPREISE UND IHRE AUSWIRKUNGEN AUF DIE BINNENSCHIFFFAHRT (IWT)

ROHÖL

Die Terminmärkte deuten auf einen raschen Anstieg der Öl- und Gaspreise im Jahr 2022 hin (55% bzw. 147%) und dann auf einen Rückgang im Jahr 2023, wenn sich die Versorgung anpasst. Für die Binnenschifffahrt haben hohe Ölpreise eine doppelte Wirkung. Auf der Nachfrageseite führen sie zu einer geringeren Beförderungsnachfrage nach Erdölerzeugnissen, während auf der Angebotsseite hohe Ölpreise zu höheren Kraftstoffkosten führen, die mindestens ein Viertel der gesamten Betriebskosten in der Binnenschifffahrt ausmachen.

ABBILDUNG 2: ROHSTOFFPREISINDIZES (2016 = 100) *

Quelle: IWF (April 2022)

* Kohle umfasst südafrikanische und australische Kohle. Getreide umfasst Weizen, Mais, Reis und Gerste. Metalle umfassen Kupfer, Aluminium, Eisenerz, Zinn, Nickel, Zink, Blei und Uran. Rohöl: Einfacher Durchschnitt von drei Spotpreisen (Dated Brent, West Texas Intermediate, Dubai Fateh).

KOHLE

Der sprunghafte Anstieg der Kohlepreise im Jahr 2022 spiegelt einen starken Aufwärtstrend bei der Kohlenachfrage wider, der auf das angespannte Verhältnis zwischen Angebot und Nachfrage sowie auf den von der EU verhängten Importstopp bei russischer Kohle zurückzuführen ist. Bereits im Jahr 2021 hat der Kohletransport auf dem Rhein aufgrund der hohen Gaspreise um fast 29% zugenommen (siehe Kapitel 2).

Im Jahr 2020 deckte Russland 55% der Kohleeinfuhren der Europäischen Union und 16% des Weltkohlebedarfs.3 Im Falle einer anhaltend hohen Kohlenachfrage und einer Blockade der russischen Kohle in den kommenden Jahren könnte die Kohlenachfrage durch Importe aus anderen Kohlelieferländern wie Australien, den Vereinigten Staaten, Kanada und Südafrika gedeckt werden.

Auch der Kohletransport auf der Donau war teilweise auf Kohle aus Russland angewiesen. Dies galt auch für die Stahlindustrie in Ungarn. Die logistische Kette, die russische Kohle über den Seehandel und den Hafen von Constanţa nach Ungarn brachte, wurde jedoch 2022 aufgegeben und durch eine Transportkette ersetzt, die den Seehafen Koper in Slowenien und den Hinterlandtransport auf der Schiene einschloss.

GETREIDE

Nach Angaben des IWF zu den Rohstoffpreisen,4 sind die Preise für alle Getreidesorten zwischen 2020 und 2022 um rund 85% gestiegen, was auf die steigende Nachfrage nach Lebensmitteln während der Covid-Krise und den Krieg in der Ukraine zurückzuführen ist.

Die Ukraine ist einer der weltweit wichtigsten Exporteure von Getreide und Ölsaaten. Nach Angaben von Eurostat5 importierte die EU-27 im Jahr 2021 8,0 Millionen Tonnen Getreide aus der Ukraine und 1,1 Millionen Tonnen aus Russland. Die Getreideexporte über ukrainische und rumänische See- und Flusshäfen sind für die Ernährungssicherheit in Nordafrika, Asien und dem Nahen Osten von entscheidender Bedeutung.

Der Krieg in der Ukraine wirkt sich negativ auf die Ernte- und Exportmengen für Getreide aus Russland und der Ukraine aus. Der Getreideexport über die Seehäfen am Schwarzen Meer macht 98% aller ukrainischen Getreideexporte aus. Für die Ausfuhr von Getreide aus der Ukraine müssen alternative Exportrouten gefunden werden. Ein solcher Weg ist die Eisenbahnlinie nach Rumänien. Die Kapazität der Bahnlinie kann jedoch die großen Mengen, die über die Seehäfen exportiert werden, nicht abdecken.6

Zu den Lösungen für den Getreideexport aus der Ukraine gehören der Transport per Bahn und Straße zu den ukrainischen Flusshäfen Reni und Izmaïl, zum moldawischen Flusshafen Giurgiulești und zu rumänischen Flusshäfen wie Brăila oder Galați. In diesen Häfen kann das Getreide dann auf Flussschiffe oder auf kleine Seeschiffe verladen werden. Im ersten Fall können Flussschiffe das Getreide bis zum Seehafen Constanța transportieren, wo es auf Seeschiffe mit großer Kapazität verladen wird. Im zweiten Fall können kleine Seeschiffe das Getreide zwischen den Flusshäfen und den Zielorten in Nordafrika mit oder ohne weiteren Umschlag in Constanța transportieren.

In Bezug auf den Schienentransport von Getreide zu den oben genannten Häfen ist zu erwähnen, dass es Unterschiede in der Spurweite zwischen der Ukraine und den meisten Teilen der EU-277 gibt. Dies gilt jedoch weder für die ukrainischen Häfen Reni und Izmaïl,8 noch für den Hafen Galați in Rumänien, der mit der gleichen Breitspur wie in der Ukraine ausgestattet ist.

Die Getreideeinfuhren für die nordafrikanischen Länder werden auch durch Ausfuhren aus den Ländern der mittleren Donau (Ungarn, Serbien) über den Wasserweg auf der Donau und den Seeverkehr zwischen Constanţa und Nordafrika gedeckt. Als Reaktion auf steigende Getreidepreise und geringere Einfuhren aus der Ukraine hat Ungarn jedoch im März 2022 Ausfuhrkontrollen für Weizen eingeführt. In Serbien wurde im selben Monat eine Ausfuhrkontrollregelung mit Quoten eingeführt. Diese Regelung umfasst Ausfuhrkontrollen für Weizen, Mais, Mehl und raffiniertes Sonnenblumenöl. Dies kann als Reaktion auf eine erwartete Verknappung von Sonnenblumenöl aufgrund geringerer Importe aus der Ukraine gesehen werden.

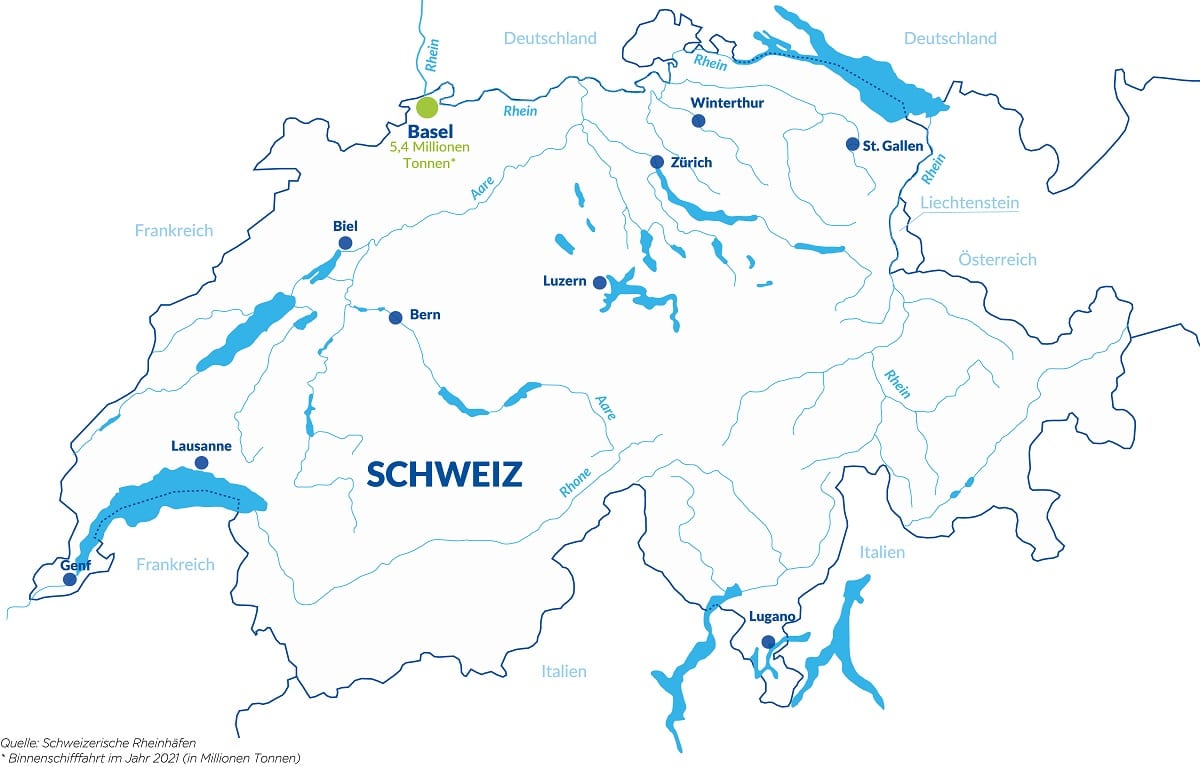

• Der Güterverkehr auf dem Rhein spielt für die Schweiz eine wichtige Rolle. Rund 25% aller von der Schweiz importierten Mineralölprodukte werden über den Rhein geliefert.

• Der Passagierverkehr auf den europäischen Binnenwasserstraßen ist ein Sektor, in dem die Schweiz eine wichtige Rolle in Europa spielt. Dies spiegelt sich in hohen Beschäftigungs- und Umsatzzahlen sowie in einer hohen Anzahl von Schweizer Flusskreuzfahrt- und Ausflugsschiffen wider.

DIE BINNENSCHIFFFAHRT IN DER SCHWEIZ

ENTWICKLUNG DER BINNENSCHIFFFAHRT IN DEN SCHWEIZERISCHEN RHEINHÄFEN IN BASEL

Das größte Gütersegment innerhalb des wasserseitigen Güterverkehrs in den Schweizerischen Rheinhäfen sind die Mineralölprodukte, mit einem durchschnittlichen Anteil von 45% in den letzten zehn Jahren. Bei fast allen in Basel umgeschlagenen Mineralölprodukten handelt es sich um Einfuhren in die Schweiz. Der Anteil der Importrichtung lag 2021 bei 98,5%, 2020 bei 99,0% und war in den Vorjahren ähnlich hoch.

ABBILDUNG 1: JÄHRLICHER BINNENSCHIFFSVERKEHR IN DEN SCHWEIZERISCHEN RHEINHÄFEN (IN MILLIONEN TONNEN)

Quelle: Schweizerische Rheinhäfen

Die Schweiz ist bei der Einfuhr von Rohöl und Mineralölprodukten auf mehrere Verkehrsträger angewiesen. Der Modal Split-Anteil des Rheins an diesen Importen betrug 24,6% im Jahr 2020 und 23,4% über den gesamten Zeitraum von 2011 bis 2020. Pipelines hatten mit 36,7% im Jahr 2020 den höchsten Anteil. Der Grund dafür ist, dass Rohöl vollständig über Pipelines importiert wird.

ABBILDUNG 2: EINFUHREN VON ROHÖL UND ERDÖLPRODUKTEN IN DIE SCHWEIZ NACH VERKEHRSTRÄGER (IN %)

Quelle: ZKR-Analyse auf der Grundlage von Avenergy Suisse

Bei einer weiteren Differenzierung der Mineralölprodukte zeigt sich, dass der Rhein hohe Modal Split-Anteile bei der Einfuhr von Diesel und Heizöl erreicht.

ABBILDUNG 3: MODAL SPLIT-ANTEIL DES RHEINS BEI DER EINFUHR VON ROHÖL UND ERDÖLERZEUGNISSEN IN DIE SCHWEIZ NACH ART DER ERZEUGNISSE (IN %)*

Quelle: ZKR-Analyse auf der Grundlage von Avenergy Suisse. Modal Split-Anteil des Rheins an allen Verkehrsträgern (Pipeline, Schiene, Rhein, Straße, Luftweg)

Der Basler Hafen ist auch ein wichtiger Ort für den wasserseitigen Containerumschlag. Der Containertransport hatte 2019 mit über 120.000 TEU an wasserseitigem Containerumschlag einen ersten Höhepunkt erreicht. Die Covid-Krise brachte dem Containertransport nur einen geringen Verlust von 5% (Stand 2020 gegenüber dem Stand 2019). Im Jahr 2021 erholte sich der Containerverkehr und erreichte mit 121.046 TEU (+9,8% gegenüber 2020) ein neues Rekordniveau. Die Schweizerischen Rheinhäfen investieren in weitere Kapazitäten für den Containerumschlag, um die für die Zukunft prognostizierten steigenden TEU-Mengen bewältigen zu können.

ABBILDUNG 4: WASSERSEITIGER CONTAINERTRANSPORT IN DEN SCHWEIZERISCHEN RHEINHÄFEN (IN TEU)*

Quelle: ZKR-Analyse auf Grundlage der Schweizerischen Rheinhäfen

* Hinweis: Für die Jahre 2014-2017 wurden die Zahlen korrigiert, um die 20.000 TEU zu berücksichtigen, die von Lkw auf die Schiene umgeladen wurden.

INFORMATIONSBLATT BINNENSCHIFFFAHRT IN DER SCHWEIZ – JÄHRLICHE ZAHLEN

Quellen: ZKR-Analyse auf der Grundlage von Eurostat-Daten [sbs_na_1a_se_r2], [iww_go_qnave], OECD-Kurzzeitindikatoren, Donaukommission (Flottendaten)

Anmerkungen zum Informationsblatt:

„Anteil an gesamter EU“ enthält Zahlen für die EU plus Schweiz und Serbien. #) Im Gegensatz zur Verkehrsleistung kann für das Transportvolumen kein länderspezifischer Anteil berechnet werden.

Der Modal Split-Anteil ist definiert als der prozentuale Anteil der Güterverkehrsleistung der Binnenschifffahrt (in TKM) an der gesamten landbasierten Verkehrsleistung. Zu den landbasierten Güterverkehrsträgern gehören Straße, Schiene und Binnenschifffahrt. Der Straßengüterverkehr wird nach dem Territorialitätsprinzip erfasst, d. h. die Daten über den grenzüberschreitenden Straßengüterverkehr werden nach den nationalen Gebieten aufgeteilt, in denen der Verkehr tatsächlich stattfindet. Diese Grundsätze werden in der Eurostat-Reihe [tran_hv_frmod] umgesetzt.

• Die Schifffahrtsbedingungen waren in den ersten sechs Monaten des Jahres 2021 mehr oder weniger normal. Im Juli 2021 war der Rhein von Hochwasser betroffen. Im Oktober und November 2021 gab es sowohl auf dem Rhein als auch auf der Donau Niedrigwasser.

• Die Kraftstoffpreise stiegen aufgrund des starken Anstiegs der Ölpreise. Die Frachtraten stiegen ebenfalls an, wobei der Trend bei Trockengütern und Containern positiver ausfiel als bei Flüssiggütern.

Was den Hafenbetrieb betrifft, so deuten die monatlichen Daten für den wasserseitigen Güterumschlag in den größten Oberrheinhäfen auf einen leichten Erholungstrend hin, der in der zweiten Jahreshälfte 2020 begann und sich im gesamten Jahr 2021 fortsetzte. Allerdings wurde diese Erholung durch das starke Niedrigwasser im Oktober und November 2021 unterbrochen.

ABBILDUNG 1: WASSERSEITIGER GÜTERUMSCHLAG IN WICHTIGEN HÄFEN AM OBERRHEIN (IN MILLIONEN TONNEN)

Quelle: ZKR-Auswertung basierend auf Hafendaten

Bezüglich der Wasserführung zeigt Abbildung 2 Daten für den verfügbaren Tiefgang bei Kaub (x-Achse) und die an der Schleuse Iffezheim erfassten Frachtmengen in Millionen Tonnen (y-Achse). Die Werte des verfügbaren Tiefgangs wurden aus den Wasserständen berechnet.2

Wenn der verfügbare Tiefgang unter eine bestimmte Schwelle fällt, werden die Schifffahrtsbedingungen zu einem Engpass für den Güterverkehr. Beispiele hierfür sind die Niedrigwasserperioden im Oktober und November 2018, aber auch die jüngere Periode Ende 2021 (siehe linker Teil von Abbildung 2). Bei Tiefgangswerten über einem bestimmten Schwellenwert zeigt das Streudiagramm keinen Zusammenhang, außer im rechten Teil des Diagramms, wo hohe Wasserstände den Güterverkehr tendenziell verringern.

ABBILDUNG 2: VERFÜGBARER TIEFGANG BEI KAUB UND GÜTERVERKEHR DURCH DIE SCHLEUSE IFFEZHEIM AM OBERRHEIN (MONATLICHE DATEN M1/2004-M12/2021)

Quelle: ZKR-Berechnung auf der Grundlage von Daten der Wasserstraßen- und Schifffahrtsverwaltung des Bundes (WSV), bereitgestellt von der Bundesanstalt für Gewässerkunde (BfG)

Für die Donau sind monatliche Daten für die Schleuse Wildungsmauer bei Wien verfügbar (Januar 2004 – November 2021). Diese Schleuse befindet sich im östlichen Teil Österreichs, wo der höchste Schiffsverkehr in der österreichischen Binnenschifffahrt zu verzeichnen ist. Im Streudiagramm ist ein gewisser Zusammenhang zwischen der Wasserführung und dem Güterverkehr zu erkennen. Wenn der verfügbare Tiefgang gering ist, scheint sich auch das Transportvolumen zu verringern.

ABBILDUNG 3: VERFÜGBARER TIEFGANG BEI WILDUNGSMAUER UND GÜTERVERKEHR AUF DER DONAU IN ÖSTERREICH (MONATLICHE DATEN M1/2004-M11/2021)

Quelle: ZKR-Analyse auf der Grundlage von Daten von viadonau und Statistik Austria

Auf der Donau war das vierte Quartal 2021 durch sehr niedrige Wasserstände und entsprechend verfügbare Tiefgangswerte gekennzeichnet. Die Ladungsverluste Ende 2021 können dadurch erklärt werden. Dies bestätigt die in Kapitel 1 gemachten Angaben.

Im ARA-Rhein-Handel folgen die Spotmarkt-Frachtraten für den Transport von Gasöl einem steigenden Trend, der im dritten Quartal 2021 beginnt und im November 2021 seinen Höhepunkt erreicht. Dies ist hauptsächlich auf die Niedrigwasserperioden im Oktober und November 2021 zurückzuführen.

ABBILDUNG 4: ENTWICKLUNG DER FRACHTRATEN FÜR GASÖL AUS DER ARA-REGION ZU ZIELORTEN AM RHEIN (INDEX 2015 = 100)*

Quelle: ZKR-Berechnung auf Grundlage von PJK International

* Die PJK erhebt Frachtraten (in Euro pro Tonne) für den ARA-Rhein-Handel mit flüssigem Massengut. Die ZKR rechnet diese Werte in einen Index mit Basisjahr 2015 um. Niederrhein: Duisburg, Köln. Oberrhein: Karlsruhe, Basel. Main: Frankfurt/M.

Das niederländische Statistikamt (Centraal Bureau voor de Statistiek, CBS) erhebt Frachtratendaten von einem Panel niederländischer Binnenschifffahrtsunternehmen. Diese Daten werden zweimal im Quartal erhoben und enthalten Treibstoff- und Niedrigwasserzuschläge.

ABBILDUNG 5: ENTWICKLUNG DER FRACHTRATEN PRO QUARTAL FÜR NIEDERLÄNDISCHE BINNENSCHIFFFAHRTSUNTERNEHMEN NACH MARKTSEGMENT (INDEX 2015 = 100, VIERTELJÄHRLICHE DATEN)

Quelle: Centraal Bureau voor de Statistiek (Binnenvaartdiensten; prijsindex)

Die Transportpreise für Trockengüter folgten ab dem dritten Quartal 2020 einem Aufwärtstrend. Die Frachtraten im Containerverkehr verzeichneten ab dem zweiten Quartal 2020 ebenfalls positive Zahlen. Bei Flüssiggütern blieben die Transportpreise auf einem niedrigen Niveau, wobei sie im dritten Quartal 2021 weiter sanken.

Die Transportnachfrage nach flüssigen Produkten stieg in den Niederlanden, nicht aber in den Nachbarländern. Dies erklärt die Situation bei den Frachtraten für Flüssiggüter für niederländische Binnenschifffahrtsunternehmen, da ihre Einsatzgebiete auch andere Länder umfassen.

ENTWICKLUNG DER TREIBSTOFFKOSTEN

Die Treibstoffkosten werden auf der Grundlage der vom Energiepreisüberwachungssystem des belgischen Wirtschaftsministeriums veröffentlichten Gasöl-/Dieselpreise analysiert.4 Ein Vergleich mit den Ölpreisen zeigt eine sehr enge Korrelation, die als Grundlage für einen Ausblick auf die Treibstoffpreise dient.

In der zweiten Hälfte des Jahres 2021 folgten die Ölpreise – und damit auch die Kraftstoffpreise – weiterhin einem steigenden Trend. Im vierten Quartal 2021 lagen sie bei 79,6 USD (ca. 69,8 Euro, da der Wechselkurs bei 1,17 USD/EUR lag).

ABBILDUNG 6: DURCHSCHNITTLICHE TREIBSTOFFPREISE NACH ANGABEN DES BELGISCHEN WIRTSCHAFTSMINISTERIUMS UND PREISE FÜR ROHÖL DER BRENT-ÖL-SORTE EINSCHLIEßLICH PROGNOSE*

Quellen: ITB und SPF Economie (Treibstoffpreis). US Energy Information Administration (Ölpreis). Federal Reserve Economic Data (historischer Wechselkurs US-Dollar/Euro). 1 Barrel (bbl) = 159 Liter.

* EIA = US Energy Information Administration. Die Prognose geht von einem nominalen Wechselkurs von 1,12 US-Dollar pro Euro in den Jahren 2022 und 2023 aus. Diese Prognosen berücksichtigen nicht die Auswirkungen des Krieges in der Ukraine.

In ihrem jüngsten kurzfristigen Ausblick vom Januar 2022 geht die US Energy Information Administration (EIA) davon aus, dass die Spotpreise für Rohöl der Sorte Brent im Jahr 2022 durchschnittlich bei rund 75 US-Dollar pro Barrel und im Jahr 2023 bei rund 67,5 US-Dollar pro Barrel liegen werden. Dies beruht auf Annahmen über die Pandemie und den wirtschaftlichen Aufschwung sowie auf OPEC-Vereinbarungen zur Drosselung der Fördermengen bis September 2022.56 Aufgrund der politischen Umstände überschritten sie Anfang März 2022 die Marke von 100 US-Dollar. Sollten sich die politischen Konflikte in der Ukraine fortsetzen, ist mit einem weiteren steilen Anstieg der Öl- und Energiepreise zu rechnen.

Die Brennstoffpreise in der europäischen Binnenschifffahrt werden sowohl von den Ölpreisen als auch vom Wechselkurs zwischen dem US-Dollar und dem Euro beeinflusst. Der enorme Anstieg der US-Staatsverschuldung begrenzt das Aufwertungspotenzial des US-Dollars gegenüber dem Euro im Jahr 2022.7 Die Abwertung des Euro gegenüber dem US-Dollar ab Mai 2021 von 1,22 auf 1,13 im Dezember 2021 führte zu einem Anstieg der Brennstoffpreise in der europäischen Binnenschifffahrt.8

Auf Grundlage dieser Überlegungen wird erwartet, dass die Brennstoffpreise in der Binnenschifffahrt im Jahr 2022 ihren Höchststand erreichen und im Jahr 2023 wieder sinken werden.

Trotz der Eindämmungsmaßnahmen im Zusammenhang mit der Pandemie zu Beginn des Jahres 2021 stieg die Beförderungsleistung (TKM) auf den Binnenwasserstraßen in der EU im ersten Halbjahr 2021 im Vergleich zum Vorjahreszeitraum um 4,3% (von 66.021 Mio. TKM auf 68.864 Mio. TKM). Die Niederlande und Deutschland, die beiden Länder mit dem höchsten Anteil an der Binnenschifffahrt in Europa, meldeten beide einen Anstieg der Verkehrsleistung um 5,5% (Niederlande) bzw. 4,7% (Deutschland).

Für den Rhein wird für die ersten drei Quartale 2021 im Vergleich zu 2020 ein Anstieg von 7,0% festgestellt. Diese positive Entwicklung ist insbesondere auf einen Anstieg der Transportnachfrage nach Kohle (+30%) und Eisenerz (+18%) zurückzuführen. Der Ausstieg aus der Kohle hat sich aufgrund der steigenden Gaspreise und der stark gestiegenen Nachfrage nach Kohle aus dem Energiesektor zeitlich verschoben. Während bei Trockengütern insgesamt ein Mengenzuwachs zu verzeichnen war, blieben die Flüssiggüter auf einem stabilen Niveau. Beim Containertransport ist für die Rheinstaaten ein Anstieg zu beobachten.

Der Passagierverkehr verzeichnete eine teilweise Erholung bei der Zahl der Flusskreuzfahrtschiffe, die bestimmte Schleusen passierten. Die Maximalkapazität der Schiffe wurde jedoch bei weitem nicht erreicht, dies stellt für die Rentabilität des Sektors eine echte Belastung dar.

Die Vorhersage der Ölpreise bleibt aufgrund der aktuellen geopolitischen Lage recht unsicher. Die Ölpreise haben Anfang März 2021 die 100-US-Dollar-Marke überschritten. Obwohl für 2022 ein Rückgang prognostiziert wird, besteht keine Gewissheit.

Ein eigenes Kapitel des Berichts ist der Schweiz gewidmet, wo Mineralölprodukte das größte Segment im Güterverkehr der Binnenschifffahrt darstellen. Der Modal Split-Anteil des Rheins an den schweizerischen Importen von Mineralölprodukten beträgt 24%, während Pipelines mit 36% im Jahr 2020 den höchsten Anteil haben.

Im Passagierverkehr der Binnenschifffahrt hat die Schweiz einen hohen Anteil. In diesem Sektor macht der finanzielle Umsatz der Schweizer Unternehmen 25,1% des gesamten Umsatzes aus, der in der EU und in der Schweiz erzielt wird. Schweizer Unternehmen sind in der Flusskreuzfahrt auf europäischen Flüssen, aber auch in der Tagesausflugsschifffahrt auf Schweizer Seen und auf dem Schweizer Teil des Rheins tätig.

1. GÜTER- UND PASSAGIERVERKEHR AUF BINNENWASSERSTRASSEN

• Die Verkehrsleistung der Binnenschifffahrt in der EU ist im ersten Halbjahr 2021 im Vergleich zum Vorjahreszeitraum um 4,3% gestiegen. Der Aufschwung wurde hauptsächlich durch den Trockengütersektor getragen.

• Der Passagierverkehr begann sich erst in der zweiten Jahreshälfte 2021 zu erholen. Die Zahl der Passagiere und damit die Auslastung der Kreuzfahrtschiffe blieb jedoch eher gering.

GÜTERVERKEHRSLEISTUNG IN EUROPA

VERKEHRSLEISTUNG DER BINNENSCHIFFFAHRT AUF DEM STAATSGEBIET DER EINZELNEN EUROPÄISCHEN LÄNDER – VERGLEICH ZWISCHEN DEM ERSTEN HALBJAHR 2020 UND DEM ERSTEN HALBJAHR 2021 (IN MILLIONEN TKM)*

Quellen: Eurostat [iww_go_qnave], OECD (Republik Moldau, Schweiz, Ukraine)

* Für das Vereinigte Königreich waren keine Daten verfügbar.

ABBILDUNG 1: VERKEHRSLEISTUNG DER BINNENSCHIFFFAHRT (IWT) IN EUROPA NACH REGION UND QUARTAL (IN MILLIONEN TKM)

Quellen: Eurostat [iww_go_qnave], OECD (Ukraine), Destatis (Rhein und Zuflüsse)

* Donau = TKM in allen Donaustaaten einschließlich der Ukraine

Die in Abbildung 1 dargestellte Verkehrsleistung zeigt einen stetigen Aufwärtstrend für die europäische Binnenschifffahrt, der im dritten Quartal 2020 einsetzt. Eine Abschwächung dieses Aufwärtstrends trat im dritten Quartal 2021 ein, was auf das Hochwasser im Rheingebiet zurückgeführt werden kann. Auf diesen Hochwasserzeitraum folgte eine Niedrigwasserperiode im vierten Quartal 2021.

RHEIN- UND DONAUSCHIFFFAHRT NACH GÜTERSEGMENT

ABBILDUNGEN 2 UND 3: VERKEHRSVOLUMEN AUF DEM RHEIN STROMAUF- UND -ABWÄRTS FÜR WICHTIGE GÜTERSEGMENTE (IN MILLIONEN TONNEN, FÜR DIE ERSTEN DREI QUARTALE DER JAHRE 2020 UND 2021)

Quelle: ZKR-Auswertung basierend auf Destatis

Der Güterverkehr auf dem traditionellen Rhein belief sich in den ersten neun Monaten des Jahres 2021 auf 126,4 Mio. Tonnen, gegenüber 118,1 Mio. Tonnen im gleichen Zeitraum des Vorjahres. Dies bedeutet einen Anstieg von 7,0%. Trockengüter und Containerverkehr verzeichneten höhere Mengen (+10,4% bzw. +3,7%), während der Flüssiggüterverkehr relativ stabil blieb. Der Kohletransport profitierte von den hohen Gaspreisen während des gesamten Jahres 2021. Insgesamt war die Nachfrage nach Schiffskapazitäten für Trockengüter in der zweiten Jahreshälfte 2021 recht hoch.

Für die Schleuse Iffezheim am Oberrhein lagen bereits Daten für das gesamte Jahr 2021 vor. Sie deuten ebenfalls auf einen Anstieg in den ersten neun Monaten hin (um 6,0%), der jedoch aufgrund von Niedrigwasser im vierten Quartal 2021 „abschmolz“. Für das gesamte Jahr 2021 blieb das Frachtaufkommen an dieser Schleuse stabil. Ein gegenüber dem Jahr 2020 stabiles Ergebnis ist damit auch für den gesamten traditionellen Rhein für 2021 zu erwarten.

ABBILDUNGEN 4 UND 5: VERKEHRSVOLUMEN AUF DER DONAU STROMAUF- UND -ABWÄRTS FÜR WICHTIGE GÜTERSEGMENTE (IN MILLIONEN TONNEN, FÜR DIE ERSTEN DREI QUARTALE DER JAHRE 2020 UND 2021)*

Quelle: Donaukommission – Marktbeobachtung

* Detaillierte Daten nach Gütersegmenten und Quartalen sind nur für die mittlere Donau bei Mohács verfügbar.

Auch auf der Donau profitierte der Eisenerztransport von der höheren Stahlproduktion. Der Anstieg in den ersten drei Quartalen 2021 im Vergleich zum gleichen Zeitraum 2020 beläuft sich auf 6,8%. Ein Blick auf die monatlichen Zahlen für Eisenerz zeigt jedoch, dass dieser Rohstoff im August und September 2021 aufgrund eines geringeren verfügbaren Tiefgangs der Schubverbände etwa 18-20% des Transportvolumens verlor.

Getreide folgt einer eher volatilen Transportnachfrage auf der Donau im Allgemeinen. Während die Getreidebeförderung im Jahr 2020 durch gute Ernten angekurbelt wurde, ging sie im Jahr 2021 zurück. Hierfür gibt es zwei Hauptgründe. Der erste Grund liegt in der Entwicklung auf dem europäischen Getreideexportmarkt. Ein zweiter Grund ist der Beginn der oben erwähnten Niedrigwasserperiode.

PASSAGIERVERKEHR IN EUROPA

Die Donau sowie der Rhein und seine Zuflüsse Mosel, Main, Neckar und Saar sind neben Seine, Rhône und Douro wichtige Einsatzgebiete für Flusskreuzfahrten in Europa. Allein die Donau machte im Jahr 2019, gemessen an der Zahl der Kreuzfahrtpassagiere, rund 40% des europäischen Marktes aus (ohne die Flüsse in Russland und der Ukraine). Zusammen mit dem Rhein und der Mosel, dem Main, dem Neckar und der Saar belief sich der Anteil auf etwa 80-85%.1

Ein statistischer Messpunkt für Kreuzfahrtschiffe auf dem Rhein ist die Schleuse Iffezheim am Oberrhein.

ABBILDUNG 6: ANZAHL DER FLUSSKREUZFAHRTSCHIFFE, DIE DIE SCHLEUSE IFFEZHEIM AM OBERRHEIN PRO HALBJAHR PASSIEREN

Quelle: Deutsche Wasserstraßen- und Schifffahrtsverwaltung

ABBILDUNG 7: ANZAHL DER FLUSSKREUZFAHRTSCHIFFE, DIE DIE SCHLEUSE IFFEZHEIM AM OBERRHEIN PRO MONAT PASSIEREN

Quelle: Deutsche Wasserstraßen- und Schifffahrtsverwaltung

Bei der Analyse der Monats- und Halbjahreszahlen für 2020 und 2021 zeigt sich, dass sich die anhaltende Erholung im Kreuzfahrtsektor ausschließlich auf den Zeitraum zwischen Juli und Oktober konzentriert. Die wichtige Frühjahrssaison konnte in den Jahren 2020 und 2021 keine Aktivität entfalten.

Für die Donau liegen Daten für die Schleuse Jochenstein bei Passau und die Schleuse Gabčikovo bei Bratislava vor. Letztere befindet sich an der Grenze zwischen der Slowakei und Ungarn. Außerdem liegt sie zwischen Wien und Budapest. Daher spiegeln die vorbeifahrenden Kreuzfahrtschiffe die Kreuzfahrtaktivität zwischen zwei wichtigen Zielen im europäischen Flusskreuzfahrtsektor wider. Neben Wien und Budapest ist auch Passau ein wichtiger Ort, an dem Kreuzfahrtschiffe ihre Reise beginnen und beenden.

ABBILDUNG 8: ANZAHL DER FLUSSKREUZFAHRTSCHIFFE, DIE DIE SCHLEUSE JOCHENSTEIN BEI PASSAU AUF DER OBEREN DONAU PRO MONAT PASSIEREN

Quelle: Deutsche Wasserstraßen-und Schifffahrtsverwaltung

Im Jahr 2019 passierten 3.668 Kreuzfahrtschiffe die Schleuse Jochenstein, mit insgesamt 512.458 Passagieren an Bord. Im Jahr 2020 waren es 324 Schiffspassagen und 25.160 Passagiere.

Im Jahr 2021 war mit 1.255 Kreuzfahrtschiffen und 107.727 Passagieren eine Erholung zu verzeichnen.

Die Daten für die Schleuse Gabčikovo zeigen für die ersten drei Quartale 2021 eine Erholung der Passagierzahlen im Vergleich zu 2020 um 77,4%. Allerdings liegt die Aktivität im Jahr 2021 immer noch 63,9% unter dem Niveau vor der Pandemie. Insgesamt wurden an diesem Grenzpunkt im Jahr 2021 (Q1+Q2+Q3) 98.000 Passagiere auf Kreuzfahrtschiffen gezählt, verglichen mit 55.000 in Jahr 2020 (Q1+Q2+Q3) und 568.000 Passagieren im Jahr 2019 (Q1+Q2+Q3). Im gesamten Jahr 2019 wurden in Gabčikovo 720.800 Passagiere gezählt.

TRANSPORTVOLUMEN IN DEN WICHTIGEN EUROPÄISCHEN BINNENSCHIFFFAHRTSLÄNDERN

ABBILDUNG 9: TRANSPORTVOLUMEN IN DEN WICHTIGEN EUROPÄISCHEN BINNENSCHIFFFAHRTSLÄNDERN (IN MILLIONEN TONNEN, VIERTELJÄHRLICHE DATEN ZUM TRANSPORTVOLUMEN AUF DEM GEBIET DES JEWEILIGEN STAATES)

Quelle: Eurostat [iww_go_qnave]

Aufgrund der mangelnden Plausibilität der Stat.Bel-Daten ab dem ersten Quartal 2018 wurden die Daten für Belgien ab diesem Quartal neu berechnet. Dazu wurde die Veränderungsrate angewendet, die in den plausibleren Daten der flämischen Wasserstraßenverwaltung (De Vlaamse Waterweg) enthalten ist. Die Reihe für Belgien folgt damit dem Trend für Flandern, ist aber auf einem höheren Niveau angesiedelt. Gegenüber früheren Ausgaben wurde beschlossen, Serbien hinzuzufügen, da die Binnenschifffahrt in diesem Land in jüngster Zeit stark gewachsen ist.

TROCKENGÜTER-, FLÜSSIGGÜTER- UND CONTAINERTRANSPORT IN DEN WICHTIGEN BINNENSCHIFFFAHRTSLÄNDERN UND -REGIONEN

ABBILDUNG 10: TROCKENGÜTERTRANSPORT (IN MILLIONEN TONNEN)

ABBILDUNG 11: FLÜSSIGGÜTERTRANSPORT (IN MILLIONEN TONNEN)

ABBILDUNG 12: CONTAINERTRANSPORT (IN MILLIONEN TONNEN)

Quellen: Eurostat [IWW_GO_QCNAVE], Destatis, Centraal Bureau voor de Statistiek, De Vlaamse Waterweg, SPW Service Public de Wallonie, Voies Navigables de France, Rumänisches Institut für Statistik

Hinweis: Für Belgien-Wallonien liegen keine unterjährlichen Containerstatistiken in Tonnen vor. Es wurde davon ausgegangen, dass die Produktgruppe „Maschinen/Sonstige Güter“ hauptsächlich aus dem Containerverkehr besteht. Die Daten enthalten die gesamte Binnenschifffahrt auf dem Gebiet des Landes/der Region.

1. SETTING THE SCENE – WHAT IS THE SITUATION TODAY?

Inland navigation is today at a crossroads, facing several influencing factors. These embrace water levels and hydraulicity issues, difficult macroeconomic conditions, i.e. slowdown in world trade, evolving sectoral, industrial and economic trends, the structural decline of carbon-related cargo and – most recently – the Covid-19 crisis. It is therefore essential to think about the development of new markets for inland waterway transport (IWT). This report will shed light on these opportunities, and on the drivers and barriers related to them.

A new market can be described as a branch where inland navigation is either not yet present or in an early stage of development and could be considered in the coming years as a suitable transport solution. However, existing markets also see innovative changes and are showing growth potential, for instance in light of energy transition and the sustainability pressure.

To develop this report, qualitative and quantitative research was carried out. Within the more quantitative part, desk research was used to analyse new markets for IWT that show growth potentials. This part entailed also the analysis of statistical data on the development of these new markets. Within the more qualitative part, interviews with relevant experts and actors from different sectors (logistics in general, IWT, ports, science and universities) were carried out, in order to gain further insight into the suitability of these new markets for IWT. This approach has led to the identification of three main pillars for IWT development.

These include urban logistics, new cargo flows triggered by energy transition (transport of alternative energies, e.g. biomass and biofuel, hydrogen, components such as wind turbines) as well as the circular economy and transport of waste. These three fields are interrelated and partly overlap. An example would be the transport of household waste in an urban agglomeration which would then be recycled to serve as a new energy which would again be transported on an inland vessel. This case would apply to all the three fields simultaneously.

Those three pillars show promising potential for IWT development. Another market that could be a growing segment in IWT in the future is the short distance container transport.1

For each of the three pillars, the report will present real-world examples or projects where inland waterway transport is already involved. In addition to that, some interesting research or pilot projects that test the integration of IWT in innovative urban waterway transport will be presented. It is worth noting that the projects presented in this report should not be considered as an exhaustive list. A more detailed annex with additional relevant projects is also available. The report will also highlight the barriers and drivers for the development of new markets in IWT.

EXISTING MARKETS FOR INLAND WATERWAY TRANSPORT – STATE OF PLAY2

Before embarking on an analysis of these identified pillars and related new markets, it is necessary to summarise the current state of the most relevant markets for IWT to understand where or where not to expect more growth. This endeavour will help to understand the need for new markets. The three main cargo segments in IWT embrace dry cargo, liquid cargo as well as container transport. In its present structure, IWT rather relies on traditional market segments. The future trend developments differ within the three main categories. Passenger transport (ferry transport, other public waterway transport, day trips, river cruises) is also an important component of IWT transport which, while having suffered greatly from the Covid-19 crisis, has seen positive demand trends in the past decades.

Overall, it is seen that the energy transition will have an important effect on freight volumes in inland navigation. This concerns coal in particular. Liquid mineral oil products will continue to be an important component of the energy sector and of inland navigation for the next decade, but a gradual decline is underway. For chemicals, the outlook is far more positive. Regarding foodstuffs, it is expected that a certain reduction of emission intensive livestock activities, combined with a change in consumer habits, will influence the transport of feedstuff. The more trade-related cargo segments (in particular container transport) will be influenced by structural slowdowns in world trade. A more detailed analysis per market segment is provided in this chapter.

DRY CARGO

The dry cargo segment accounts for 59.8% of IWT volume in EU-27 in 2020 and can be further sub-categorised into five segments:

Agricultural products

Agricultural and food products currently have a share of around 9% of goods transport on the Rhine and around 16% of goods transport on the Danube. Agricultural products show strong correlation with harvest results, a correlation that dominates the volumes transported each year. Bad harvest results lead to a decrease in volumes transported, good harvest results increase transport volumes. IWT seems to be a preferred mode of transport for long-distance transport of agricultural goods.

Feedstuff and food products

In western Europe, densely populated areas such as the Netherlands and Belgium are experiencing problems with high nitrogen emissions, due to intensive livestock activities. Political pressure to reduce these emisisons could lead to a reduction of these activities in western Europe. Additional influencing factors for this trend stem from a change in consumer habits towards less meat consumption. In the case of a reduction of livestock activities in western Europe, a shift of these activities to other parts of Europe (eastern Europe) or to overseas countries (South America) is likely.

In both cases, food products such as meat would then need to be imported, which would create transport activities. The case whereby these products are transported by inland vessels, however, is not very likely. The feedstuff needed for feeding cattle (livestock activities) would no longer be transported in the same volumes in western Europe, which would reduce transport demand, also on inland waterways. Therefore, the current trends in this sector point to a reduction of feedstuff transport in the future in western Europe.

A completely different market is the transport of food products in cities, which is beginning to develop, and which will be dealt with in this report as a new market in IWT, and illustrated by some successful projects (e.g. in Paris and Ghent).

Iron ore, steel and metals

Iron ore, steel and metals represent an important segment for inland navigation. For the Rhine their share accounts to 25% of total goods transported and for the Danube, the share reaches even around half of total goods transported.

For western Europe, the transport demand outlook for iron ore is not growth orientated, due to a high environmental pressure to reduce emission intensive steel manufacturing processes for which iron ore and coaking coal are needed as raw materials. Iron ore transport is also very vulnerable to macroeconomic fluctuations and a reduction of world trade, as steel production reaction is very sensitive to these factors. This was once again shown during the Covid-19 crisis.

Apart from these environmental and cyclical factors, iron ore and steel demand seem to be more saturated in western Europe than in eastern Europe. This last point is related to long-term economic catch-up mechanisms in eastern Europe. For the Danube region, these catch-up mechanisms contribute to a more growth-oriented outlook for steel and iron ore.3

Sand, stones, gravel and building materials

A main positive trend is captured in the segment of sands, stones, gravel and building materials, possibly more pronounced in western Europe than in eastern Europe. This consists in a growing activity in the housing market, in parallel with demographic growth. The last-mentioned factor divides western Europe, where demographic projections are positive (in particular in France, the Netherlands and Belgium) from eastern Europe, where they are more orientated towards stagnation or even a decrease.

For western Europe, a concentration on larger waterways (consolidation process) is likely to take place, in parallel with a concentration on larger production sites within the construction sector itself. In the coming years, in western Europe, large volumes of sand and gravel are expected to come on the market as a result of dredging and the great need of materials for dike reinforcement. Untapped potentials lie in the urban inland waterway transport and transport of construction materials to construction sites. This urban transport of building materials is one example of a new market in IWT. Therefore, this market segment comprises both traditional long-distance transport as well as new urban short-distance transport.

Coal

Coal faces an almost complete phase- out in western Europe, as far as steam coal (hard coal used in the energy sector) is concerned. The reason is the energy transition in the major IWT countries in western Europe. Indeed, among other measures, with the exit from coal, governments aim to reach the goals of the Paris Agreement of the United Nations, adopted by 196 parties on 12 December 2015 and which entered into force on 4 November 2016.4 In Germany, for instance, the government decided on a gradual exit from hard coal until 2035 and lignite until 2038.5 For coal transport in IWT, only hard coal is relevant as lignite is not transported on inland waterways.

Figure 1 shows the decrease in coal transport in the EU-27 that started in 2015. Around 90% of the series ‘Coal and lignite, crude petroleum and natural gas’ concerns hard coal, as neither lignite, nor crude petroleum or natural gas are transported on inland waterways in large quantities. And within this amount of hard coal barge transport in the EU (27.4 million tonnes in 2019), 84.8% was transported on German inland waterways (23.3 million tonnes). One could also mention that coal transport by inland vessel is even higher in the Netherlands (25.3 million tonnes in 2019) than in Germany, but these similarly high numbers reflect the fact that coal is transported from the Amsterdam-Rotterdam-Antwerp (ARA) seaports in the Netherlands to Germany, for providing coal fired power plants and the steel industry with raw materials.

The amount of 27.4 million tonnes of hard coal barge transport in the EU does not contain coking coal or coke (2.5 million tonnes in 2019). The entire coal volume on EU inland waterways is therefore around 30 million tonnes per year. The coal transport by inland vessels in Germany represents around 84% of total coal transport by inland vessels in the EU.

FIGURE 1: TRANSPORT OF FOSSIL FUELS BY IWW IN THE EU 27 BETWEEN 2008-2020 (MILLION TONNES)

Source: Eurostat [iww_go_atygo]

However, hard coal is at the beginning of a phasing-out process in the energy sector in Germany. Figure 2 shows the planned reduction of power plant capacities for hard coal (in GigaWatt) in Germany. The first power plants were taken off the grid in 2020, and already by the end of 2024, the original power plant capacities will have been halved. Based on this series, a complete phase-out of steam coal transport on German inland waterways can be expected by 2036.

Steam coal is the type of coal used in the energy sector, while coking coal or coke is the type of coal used in the steel industry. Based on the Eurostat data, the large majority of hard coal transport in the EU would be steam coal (27.4 million tonnes), and only a small fraction would be coking coal (2.5 million tonnes). However, evidence about the use of coal in Germany points to a much higher share of coal used for steel manufacturing (according to coal import statistics, coal used for steel production accounts for at least 50% in Germany). The classification within the Eurostat NST 2007 system might not reflect this pattern entirely.

FIGURE 2: REDUCTION OF POWER PLANT CAPACITIES FOR HARD COAL IN GERMANY (GIGAWATT)

Source: Bundesministerium für Umwelt, Naturschutz und nukleare Sicherheit

At present, the Danube area is less affected by the energy transition, as it is progressing at a slower pace in this region. However, it is expected that all IWT regions will be impacted by the energy transition developments in the near future.

The series ‘Coke and refined petroleum products’ will be discussed in the next part on liquid cargo. It has to be clarified that this NST 2007 group contains mainly refined petroleum products (share of 97%), while coking coal is represented only marginally in this series with 3%.

Liquid cargo (chemicals and petroleum products)

Volumes of liquid cargo account for 28.1% of the IWW transport volume in EU-27. A main distinction must be made between chemicals and refined petroleum products. On the Rhine, the share of petroleum products is very high with 17.3% of total cargo transport in 2020, and 27.6 million tonnes in absolute numbers, forming the largest cargo segment on this most important inland waterway in Europe. Petroleum products are also very important for IWT volumes in Belgium and the Netherlands.

Although petroleum products such as gasoil/diesel, gasoline and kerosine are still expected to be part of a propulsion mix in the next decade, there are no growth prospects, and a gradual decline is assumed, possibly reaching near zero by 2050. Indeed, the long-term vision of “a zero GHG emissions inland navigation sector by 2050” is a shared political goal at various levels.6 Electrification of the transport sector, which makes petroleum products gradually redundant, acts as another influencing factor that puts pressure on liquid cargo volumes in IWT.

For chemicals, a far more growth-oriented development is expected. IWT is the preferred mode of transport in the chemical industry, and chemical production itself has overall more growth prospects in Europe than mineral oil production.

Petroleum products have lost some transport performance in recent years (mainly due to low waters and the Covid-19 crisis), but there was no real downward trend so far in this segment (see figure 1, series ‘Coke and refined petroleum products’). However, a significant drop in this segment would prevail in the case of a major electrification of road transport. The reason is that liquid fossil fuels used in the road transport sector, together with heating oil, form the backbone of the petroleum products transport in IWT.

Electrification of the European transport sector is still in an early phase, allowing the IWT sector to adapt and explore new market opportunities. For instance, in 2019, the share of electric cars within the total number of new registered cars was 1.6% in Germany, 1.0% in France, 0.8% in Belgium, 11.4% in the Netherlands and 2.1% in Switzerland.7 For Germany, national figures for 2020 (for other countries, Eurostat figures were not yet available for 2020) point to a strong increase of this share up to 6.6%.8

According to these national data, a major absolute increase of newly registered electric cars can be observed in Germany in 2020 (194,163 units) representing a major uptake compared to 2019 (63,281 units). However, this number is very low compared to the stock of cars (47.716 million units in 2020) in this country, of which the vast majority is still propelled by liquid fossil fuels.

Also in Europe overall, new registrations of electric cars have shown strong increases both in absolute and relative terms. According to the European Alternative Fuels Observatory (eafo), new registrations of electric cars in 2021 amounted to 16% of all newly registered cars, whereas the value for 2020 was far below at only 10.5% and 3.0% in 2019.9

Altogether, the very recent uptake in electric cars registration can explain why liquid petroleum products has not experienced any clear structural downward trend within inland waterway transport to date. However, electrification of the transport sector is currently gaining momentum, also underlined by a further rise in the share of new electric cars in the first seven months of 2021 (reaching 10.7% of all new registered cars) in Germany.10 The trend in Germany is of high relevance, as the Rhine market represents – together with the ARA region market – the core region of the liquid cargo transport in Europe.

Container

Container transport accounts for 12.1% of IWW transport volumes in the EU-27. Already before the Covid pandemic in 2020, the world trade of goods slowed down, and this trend is expected to continue. The importance of global trade in goods is decreasing in trend terms, while trade in services is increasing. This structural change in trade can be explained by the following factors:11

1) Shift of consumer demand away from tradeable goods to services in developed countries (dematerialisation).

2) Growing incomes and wages in emerging market countries leading to less wage and cost differentials worldwide, and therefore to less incentives for worldwide trade of goods.

3) Technical innovations such as 3-D printers reducing trade in goods further.

Further reasons taken from van Dorsser et al (2018)12 for the structural change in container throughput are:

4) Declining population growth in Western Europe.

5) The fraction Labour/ Population, i.e. the share of population contributing to economic output is decreasing, not only due to ageing populations but also due to the retirement of the baby boom generation. In addition to that, job losses linked to artificial intelligence put approximately 40-50% of jobs at risk.

6) The growth rate of the fraction GDP/Labour decreases, which reflects a decreasing productivity growth, resulting from lower economies of scale in innovations. This trend affects technology frontier countries.

7) Reverse globalisation (decreasing ratio Trade/GDP), i.e. a higher focus on local production.

8) Containerisation coming to its saturation limits.

These tendencies would create more regional logistic and production chains and would certainly have negative effects on seaborne container transport, as around 90% of world trade in goods is carried out by seaborne trade. Furthermore, these trends would affect seaport hinterland container transport on inland waterways. This is because inland waterway container transport is strongly linked to maritime container transport. However, if container transport would be able to integrate more in regional and urban logistics chains, and if it would be possible to build up short-distance container transport, it would keep a higher growth rate overall.

PASSENGER TRANSPORT

Passenger transport demand can be split into touristic activities and public transport activities. The latter also includes the traditional ferries, crossing waterways transversely in the form of floating bridges. This characteristic plays a crucial role in urban mobility. During the pandemic, the touristic passenger transport came to a complete halt. The relaxation of sanitary measures is expected to lead to a slow recovery in this market. It might take some years before the demand reaches its pre-crisis level.

Passenger transport in the form of public transport services, including ferries, on urban waterways can be considered as an important tool for making cities greener and more sustainable. The fact that urban passenger transport on waterways can be carried out by electric propulsion, given the limited distances in cities, is one major reason for its potential for making cities more environmentally friendly. At the same time, waterway transport reduces the overutilisation of roads and related negative effects (accidents, traffic jams in cities). Passenger transport in cities in the form of public transportation systems has huge potential, as the example of the waterbus in Brussels shows. The present report will focus only on public passenger transport in cities, not on touristic transport.

UNTAPPED POTENTIAL FOR INLAND WATERWAY TRANSPORT – MAIN DRIVERS

The following chapter will analyse the main trends that are expected to act as driving forces for urban mobility. As will be seen, the characteristics of inland navigation make it suitable as an alternative transport solution in urban areas in light of the current challenges that urban environments are facing. New markets in inland navigation can therefore emerge in light of climate policies favouring the decarbonisation of societies and insisting on more sustainable, resilient and future proof transport modes. IWT could therefore play a crucial role for making societies, in particular cities, more sustainable from an environmental and social point of view, resulting in new market opportunities. The social point of view refers to a reduction of accidents and noise by a modal shift from road to IWT, and a reduction of related negative externalities.

SATURATION OF EXISTING TRANSPORT INFRASTRUCTURE IN CITIES

Nowadays, large agglomerations are facing important challenges at the demographic, economic and environmental levels. Currently, more than half of the world population lives in urban areas and this share will increase further in the future. The World Urbanisation Prospects of the United Nations Department of Economic and Social Affairs (see figure 3) projects that this percentage will increase to 68% by 2050. In the EU, urbanisation rates are among the highest in the world. Around 74% of the EU population already lives in urban areas. The share of urban population reaches for instance 98% in Belgium and 91% in the Netherlands, both countries being important for European IWT. Other relevant IWT countries such as France, Germany and Romania are projected to see a steady decrease in their rural population by 2050.

FIGURE 3: SHARE OF URBAN AND RURAL POPULATIONS IN EUROPE BETWEEN 1950 AND 2050 (% OF TOTAL POPULATION)

Source: World urbanisation prospects – United Nations, Department of Economic and Social Affairs, Population Division (2018)

The demand for goods, of which cities are net importers, rises with the size of urban population. In parallel, the production of waste increases and solutions to remove such waste must be found. This also leads to an increase in the demand for transport infrastructure. For this reason, the EU is dedicated to promoting sustainable urban transport systems. Traffic congestion in cities is the cause of substantial economic loss, estimated to account for EUR 180 billion per year in terms of delay costs and about EUR 32 billion per year in terms of deadweight loss at EU-27 level.13 According to the Staff Working Document of the Smart and Sustainable Mobility Strategy, ‚[t]he delay cost gives a value of the travel time lost relative to a free-flow situation. The deadweight loss costs is the part of the delay costs which is regarded as a proper basis for transport pricing.‘

Current transport systems are mainly based on fossil fuels and are therefore not sustainable in the long run, given the related negative externalities, scarcity of resources and energy dependence of the EU.14 Road transport is by far the dominant mode of transport and represents 76.3% of total inland freight transport (excluding pipelines) in the European Union, compared to 17.6% for rail transport and 6.1% for inland waterway transport. In some countries, IWT has a higher modal share than rail transport, such as in the Netherlands and in Belgium.

Changing habits among consumers places another strain on urban logistics. The rise of e-commerce and the necessity of ever faster and personalised deliveries incentivise the fragmentation of deliveries, leading to 23% of vehicles on the road travelling unloaded, according to a case study conducted in Austria.15 The increase in the number of vehicles is also linked to the phenomenon of logistics sprawl, whereby, due to high land costs in the urban perimeter, logistics operators prefer to move their sorting centres further and further away from the centre. These elements put additional pressure on environmental indicators in large agglomerations, as they lead to even more road transport.16 Innovative solutions for urban freight delivery are called for to avoid the negative impacts that this framework would cause either to the economy and to the environment.

Cities located near and around waterways could take advantage of their location to make deliveries of goods in specific sectors more efficient and less polluting, through an increased use of IWT solutions. Moreover, due to historical reasons, inland waterways are often located in the heart of city centres. This feature makes them a natural infrastructure suited to deliver transport services of different types (goods for shops, restaurants, hotel and accommodation, etc.) in areas that are more and more precluded to road transport.

Contrary to road freight, IWT is an unsaturated mode of transport, as it uses transport infrastructure with free capacities, and a safer mode of transport. The lack of congestion facilitates on-time deliveries and the overall efficiency of urban transport flows, while generating fewer accidents and fatalities and consequently reducing the related negative external costs (health treatment costs, societal costs due to fatalities).

GREENHOUSE GAS AND POLLUTANT EMISSIONS OVERALL AND IN SELECTED CITIES

The transport and storage sector (NACE H) is responsible for approximately 15% of total greenhouse gas emissions in the EU and has not seen a significant decline in this respect as other polluting sectors, as shown in Figures 4 and 5.17

FIGURE 4: GREENHOUSE GAS EMISSIONS – DEVELOPMENT AS INDEX IN THE EU-27 (INDEX 2008 = 100)

Source: CCNR elaboration based on Eurostat data [env_ac_ainah_r2]

FIGURE 5: ABSOLUTE DEVELOPMENT AND STRUCTURE OF GREENHOUSE GAS EMISSIONS IN THE EU-27

Source: CCNR elaboration on Eurostat data [env_ac_ainah_r2]

Alongside GHG emissions, air pollutant emissions are also very problematic. The very small particles, known as PM10, common air pollutants, are inhalable and can cause health problems. For this reason, the EU sets the limit that PM10 emissions in cities must not exceed 50 µg/m3(daily average concentration) on more than 35 days per year. Figure 6 shows the 36th highest PM10 emission value per year as average of a constant panel of air quality stations in each city18 for Amsterdam, Berlin and Brussels.19

In order to respect the threshold or emission limits set by the EU, the values in figure 6 should not be higher than 50 µg/m3. The values are almost always below this threshold. However, for Amsterdam and Berlin, the emission trend between 2016 and 2018 was slightly upward orientated. Figure 6 shows also that Berlin exceeded the emission limit in 2014.

FIGURE 6: YEARLY DATA FOR THE 36TH HIGHEST PM10 EMISSION VALUE FOR PARTICULATE MATTER (< 10 µM) IN SELECTED EUROPEAN CITIES BETWEEN 2012 AND 2018 (µG/M3)

Source: European Environment Agency and CCNR analysis, average air pollutant concentrations for a panel of air quality measurement stations in each city

The PM10 data for Paris were not complete (missing values for certain measurement stations in certain years) and could not be shown on a representative basis.

NO2 is another important pollutant, affecting health and air quality in cities. Figure 7 shows the annual average concentrations of nitrogen dioxide (NO2) measured at the level of a panel of air quality stations in Amsterdam, Berlin, Brussels and Paris. In Paris, the average concentration of nitrogen dioxide was constantly above the limit set by the EU, which states that the annual mean concentration of NO2 should not exceed 40 µg/m3 on more than 35 days per year. Values near the emission limit are also observed for Berlin and Brussels.

FIGURE 7: YEARLY DATA FOR THE 36TH HIGHEST EMISSION VALUE FOR NITROGEN DIOXIDE IN SELECTED EUROPEAN CITIES BETWEEN 2012 AND 2018 (µG/M3)

Source: European Environment Agency and CCNR analysis, average air pollutant concentrations for a panel of air quality measurement stations in each city

As would be expected, emission data collected by the European Environment Agency show that PM10 and NO2 levels tend to be much lower in rural areas, and on the outskirts of cities. This provides an incentive to focus efforts on reducing emissions in urban areas. Inland waterway transport – in the form of electrified urban water transport or using other clean propulsion methods – could help to reduce these emissions. The further use of low-emission vessels would be a positive contribution for enhancing air quality and reducing congestion in cities. The combination of both factors could result in growing market opportunities for IWT.

RISING PRESSURE TO IMPROVE THE SUSTAINABILITY OF OUR ECONOMIES

Addressing climate change is a political priority for institutions at all levels (international, national, and local). Public policies aiming at an emission-free economy often highlight the relevance of sustainable transport solutions. Inland navigation should play a relevant role in this transition process. The European Green Deal (EGD) 2019 calls for 75% of inland freight transport to shift from road to rail and inland waterways. Main European cities are restricting access to specific areas for heavy-duty vehicles through low-emission zones. Public policies related to the energy transition are fundamental levers for the market development of IWT. While the energy transition of the IWT sector itself is out of the scope of this report, there is no doubt that the ‚greening‘ of IWT could strengthen its position as a sustainable mode of transport – both from an environmental and an economic point of view.

New markets in inland navigation become essential in the framework of a transition towards a more sustainable transport sector and a climate neutral Europe. Inland navigation in the 21st century also faces several bottlenecks, including those that are structural, both on the demand and supply sides.

On the demand side, the outlook for several goods segments points to saturation or even decline (e.g. coal). A likely structural slowdown in world trade is another important challenge for inland waterway transport. While the energy transition changes the product portfolio of inland navigation, it is also expected to lead to the emergence of new markets, to which the inland navigation sector will need to adapt in order to gain market shares.

On the supply side, inland vessels will be confronted more and more with difficult navigation conditions on free-flowing rivers such as the Rhine, Danube, Elbe, and others. The underlying reason is low water periods which are expected to intensify with the ongoing climate change. The low water phenomenon and its related negative effects (loss of transport volume and of modal shares for IWT) calls for a diversification of the areas of operation of inland vessels, towards a higher participation in city or urban logistics, for instance, where water levels are less critical.

For these reasons, it is important to identify and anticipate the emergence of new markets in inland waterway transport (IWT). New markets can determine new types of products transported by inland vessels, but they often imply new types of logistics, new types of vessels and new areas of operation.

For example, one important new market, urban inland waterway transport, does not only imply a change in the type of cargo transported (e.g. parcels instead of mass cargo), but also a change in the areas of operation (city logistics instead of transport crossing borders), a different range of logistics (short-distance instead of long-distance transport), and different types of vessels (smaller vessels instead of large vessels).

Based on statistical data, literature research and expert interviews, the following new markets for IWT have been identified:

1) Urban passenger transport by inland vessels in the form of public local transport (examples are found in Antwerp, Brussels and Rotterdam).

2) Urban freight transport by inland vessels (construction material, food products, parcels, etc.) in large cities such as Amsterdam, London, Paris, Lyon.

3) New cargo flows stimulated by circular economy strategies (e.g. waste transport).

4) Transport of renewable energies or components for their generation (biomass, biofuel, hydrogen, wind turbines).

The detailed analysis of these topics reveals one common feature: new markets for IWT exist, and with high potentials. However, these markets are not yet sufficiently developed to gain easy access to the inland navigation sector. They are fraught with intermodal competition, commercial, logistical and technological challenges, risks and uncertainties to varying degrees.

The urban transport of freight, passengers and waste is an activity where inland navigation meets the need of society and governments to find solutions for existing and growing urban problems, in terms of saturation of road infrastructure, related negative externalities, and ecological problems in cities.

Similarly, the transport of alternative energies meets the need of our society to transform the energy sector from a fossil to a non-fossil form of energy generation. It is found that this new market, despite having certain potentials, is strongly dependent upon political and regulatory activities. Together with the partly unknown technological and economic trajectories of different renewable energies, these features represent certain risks for the development of this sector as a new market for IWT.

However, urban waterway logistics also face hurdles and risks. One significant hurdle is the competition for space in urban areas between the transport or logistics sector on the one hand, and the important housing and tourism sectors, on the other hand.

All in all, many transformations need to be accomplished to extend the cargo portfolio of inland navigation. The report sheds light on these necessary transformations and challenges and describes key projects in different new markets and in different cities, countries and regions, where these transformation processes are already underway and where first success stories can be told.

2. INLAND WATERWAY TRANSPORT EMBEDDED IN URBAN LOGISTICS

In cities situated close to waterways, inland navigation is considered increasingly in logistic supply chains. Urban logistics embraces a broad field of freight distribution comprising various interactions such as Business to Business (B2B) or Business to Customer (B2C) and the passenger transport system within urban areas.20 Sustainable urban logistics should enable the flow of goods that enter, leave and circulate in the cities to be transported in the most environmentally friendly and sustainable way.

IWT in urban logistics has found more interest in the last decade, thanks to initiatives for more sustainable urban logistics coming from the public side (cities), and from companies active in the retail or construction sector with logistical activities in cities. However, it is still far below its reasonable potential.21 This report will give an insight into both already operational projects and pilot or research projects. It distinguishes between urban passenger transport and urban freight transport.

URBAN PASSENGER TRANSPORT USING WATERWAYS

Urban passenger transport using waterways can be divided into public transport services for commuter traffic and touristic transport. There is of course a certain overlap between these two categories. Within this report, the focus will be on public transport services. For touristic transport a number of examples in cities (e.g. Amsterdam, Paris, Hamburg, etc.) exist, but this is not a new market. However, public transport by inland vessel in large agglomerations is an activity that, although not entirely new, was largely abandoned over a long time. This is the reason why it is integrated in this report as a new market.

The canal shuttle Waterbus navigates between Brussels and Vilvoorde, an approximate distance of 10 kilometres on the Zenne canal. It brings commuters, other passengers and tourists on a daily basis from remote locations to the city centre of Brussels. In only less than an hour, with a speed of 12-14 km/h on average,23 the shuttle travels from Vilvoorde Centrum, Park Dire Fonteinen, Cruise Terminal, Quai de Heembeek, Pont van Braet, Quai de Peniches, all the way to Sainctelette. The stops accessed via other public transport modes or by car have free parking places.

Waterbus illustrates an extension of the public transportation system in Brussels allowing to reach out to remote areas and interconnecting the city to a better extent. Sub centres are emerging in the different areas to attract citizens. Through Waterbus, incentives to develop sub centres are reinforced.

Launched in 2013, the Waterbus project proved its economic viability and its role as a solution to urbanisation challenges such as emissions and high road congestion and related long travel hours. It transports on average 40,000 passengers per year.24

A similar project has been implemented in Antwerp known as ‚DeWaterbus‘ connecting Antwerp to Lillo and Hemiksem.25 In the Netherlands, a waterbus project has also been implemented connecting the city of Rotterdam better via the waterways.26

Source: CCNR based on waterbus.eu/en-us and Open Street Map data

The Roboat project aims to develop autonomous sailing on waterways. Roboat is a concept born from the collaboration between the Massachusetts Institute of Technology (MIT) and the Amsterdam Institute of Advanced Metropolitan Solutions (AMS). Besides the main partners, Roboat also enjoys the support of the municipality of Amsterdam, Waternet, Torqeedo, Vetus and Murata.

Roboat aims to make use of the existing infrastructure provided by the canals of Amsterdam and is open both for freight and passenger transport. The floating platforms using self-driving technology are in fact versatile, which is a quite unique characteristic. They can be used to transport persons, collect waste, deliver goods, combine to form bridges and performance stages. According to the project’s official website, the use of Roboats as floating dumpsters carrying away waste could serve 70% of the city centre’s needs in terms of waste collection. The project is currently still in a pilot phase. With a duration of five years, the partners began testing the first small scale prototypes in 2017. In the following years, research continued and in 2020, the full-scale prototypes were developed.

Concepts such as that of Roboat have the potential to improve passenger and freight transport in cities that are deeply interconnected with inland waterways, especially since it has touched a niche in the city logistics of Amsterdam. However, regulatory obstacles hamper the full implementation. Roboat’s advantage is that its headquarters are located directly on the Amsterdam waterway, allowing them to perform real testing of the vessel on their own ‚private‘ waters to allow a better and real testing of the vessel. In general, for autonomous sailing, a boatmaster needs to be on the vessel to be allowed on public waterways.

Roboat does not consider freight transport yet, as the necessity of human interaction in this field entails increased labour costs. So far, two business cases have been assessed. The Roboat for passenger transport as a taxi carrying up to five passengers and the second relates to waste collection. Both projects show increased potential. Roboat in future could also be used as an infrastructure component of a passenger bridge for example, in congested areas.

Source: Adobe Stock, Castel Sant’Angelo and Ponte Sant’Angelo – bridge over the Tiber River, Rome, Italy

The city of Rome has shown interest in using the Tiber as a passenger transport infrastructure.

This further proves that IWW transport methods are attractive for their unexpressed potential in cities where they are far less developed. Tiber Cat is a project, yet to be implemented, on which architects Paolo Carlodalatri and Fabrizio Vinditti are working. Tiber Cat involves building a fully electric catamaran capable of carrying up to 50 passengers. It would be able to navigate with a water level of one metre, and would complement the existing public transport network, differentiating itself from existing tourist boats.

The idea is part of plan of the Italian Ministry of Infrastructure and Transport, in collaboration with the city of Rome, to redevelop the area of the Tiber to make it navigable over a 60 km stretch. The use of the catamaran would be the first step towards this long-term goal, allowing navigation on the most navigable stretches of the river (from Prima Porta to Isola Tiberina, a distance of about 10 km). This initial choice would avert the challenge posed by the rapids that characterise the Tiber, improving the chances of success. Constant support from the administration represents the necessary condition for the project to get off the ground.

Project of the catamaran, source: Professor Paolo Carlodalatri

URBAN FREIGHT TRANSPORT USING WATERWAYS

Inland navigation allows for many different types of cargo to be transported in city centres (parcels, food products, cardboard, construction material etc.) and in varying forms (pallets, bulk, barrels, containers and so on). This is demonstrated by the large number of projects (non-exhaustive) presented in this section. For each project, it is specified whether the project is already implemented or whether it is still in the pilot stage (on its path to implementation/ showing potential for sustainable urban logistics solutions).

URBAN PARCEL DELIVERY

Multimodal parcel delivery in urban areas has rooted on fruitful ground. Projects operating in various cities provide an insight into sustainable transport methods addressing urbanisation challenges.

Holland’s Glorie – DHL in Amsterdam – implemented project29

In Amsterdam, Holland’s Glorie, a retired passenger ferry, found its passengers replaced by parcels. Since 2017 Holland’s Glorie has been operating using three modes of transport, inter alia electric trucks, a vessel and cargo bikes to bring parcels to the city centre of Amsterdam.

Source: DHL

FIGURE 1: MULTIMODAL PARCEL DELIVERY IN URBAN AREAS

The ferry navigates twice a day from its base towards the city centre. Figure 1 captures the different steps of the delivery process. Parcels arrive at Schiphol airport and are loaded onto electric trucks which then transport the parcels to the vessel. Once in the vessel, the journey begins on Amsterdam’s waterways, to reach a platform in the city centre (Koningsplein) where cargo bicycles await the parcels to be delivered. In total there are 21 bicycle messengers.

The advantages of delivering by bike lie in the efficiency of deliveries by hour. One can reach up to 17 deliveries per hour, whereas by car it amounts to 5 or 6 deliveries. The reasons for this are set in the narrow streets of Amsterdam’s city centre, where traffic, many bikes, motor bikes and almost no available parking places slow down the delivery process.

Another promising and operational example of successful parcel delivery using waterways is Urban Logistic Solutions (ULS) in Strasbourg. With a rental vessel from VNF, parcels are transported from the north area of the Port of Strasbourg (Quai du Bassin des Remparts, where the warehouse is situated) to a platform located in the city centre (Quai des Pêcheurs),31 a distance of approximately five kilometres. The parcels are packed into container-like boxes, and are thereby protected from all kinds of weather conditions and from being lost.

Once arrived in the city centre, 15 available cargo bikes deliver the parcels to the final recipient in the city centre area. For the time being the vessel carries out one rotation per day but shows increasing potential in the near future. In fact, plans to invest in a larger vessel running on alternative fuel are under preparation.

A mobile crane on the platform helps transfer the loads from the vessel onto the cargo bikes. According to Thomas Castan, Director of ULS Strasbourg, cranes on the berths handle goods more efficiently and allows a better quality of transport service. In addition, an integrated crane on the boat would come with additional maintenance costs.

As well as parcel delivery, ULS transports different kinds of goods and recycles used cardboard boxes on its vessel. The capacity of the vessel amounts to 680 palettes which amount to 180 kg each. It yields a total capacity of 122 tonnes and has a width of 3.06 metres.

Source: Le Monde /Frederick Florin

In addition to the environmental and efficiency reasons fostering the use of IWT in this segment, the market of parcel delivery is also booming due to increasing online trading. Hence there is potential to expand, especially as regards last mile deliveries and usage of inland waterways. During the interview, the impact of public policy actions was also highlighted. For instance, possible changes in the access routes or possible access restrictions for trucks to the city centre could encourage some economic actors into looking for alternative transport modes, including IWT.

Created in 2016, Fludis is a new player in urban logistics. As it is fully electric, it provides competitive and decarbonised solutions for major players in transport, logistics and trade, handling the overall provision of the first and last kilometre. The aim is to avoid costly stock-outs in the warehouse. The company employs 11 people, including eight cyclists.

Fludis operates as follows: a semi-trailer truck transports the goods directly to the boat and the bikes deliver to the final customer:

– for the outbound journey, Fludis delivers for the company Lyreco in several districts of Paris every day;

– for the return journey, it collects electronic waste from Paprec.

The boat makes several stops in Paris depending on the delivery addresses. Each day, approximately 700 kg of goods are delivered. The sailing time is valued by working onboard (preparation of the packages on board: breaking down the pallets and reconstituting the loads).

Despite the advantageous position of the Seine, outstanding issues remain which could impact the viability of the project. The berths available for urban logistics in Paris are multi-purpose berths and can be used for 15 minutes only. However, this is not adapted to the specific demands of urban river logistics, as Fludis deliveries require a two-hour stay at the berth to accomplish the different deliveries. To make this possible, an adaptation of the current contractual model with Haropa, the port company managing the infrastructures of the Port of Paris, would be needed.

Fludis has to pay high dock dues compared to trucks which can circulate in Paris freely without having to pay any kind of tax. This affects its competitive position compared to other transport modes. Eventually, political and economic decision-making should have an impact on the development of urban river logistics, whether negatively (i.e. limited use of berths for transshipment operations) or positively (setting up of incentives for the use of IWT solutions in urban areas).